Office Management |

| RECEIVABLES |

|

|

|

|

CREDIT EXTENSION |

|

One employee of the dealership should be assigned authority for extending credit. This employee should not be directly associated with the sales function. If a credit card is not used by the customer, a credit application should be completed, and statements made on the application should be checked with a credit agency. Upon approval by the designated employee, the customer should be informed of the amount of his credit limit and the due date of his account. To assist in maintaining control over the extension of credit, all charges should be posted daily to the accounts receivable ledger. |

COLLECTION |

|

One employee should be assigned responsibility for follow-up and collection of accounts. In most instances, this will be the person who is responsible for extending credit. A statement of account should be mailed promptly at month end to each credit customer. When dealership collection efforts, including telephone or personal contact, are unsuccessful, consideration should be given to placing the account in the hands of a collection agency or an attorney. |

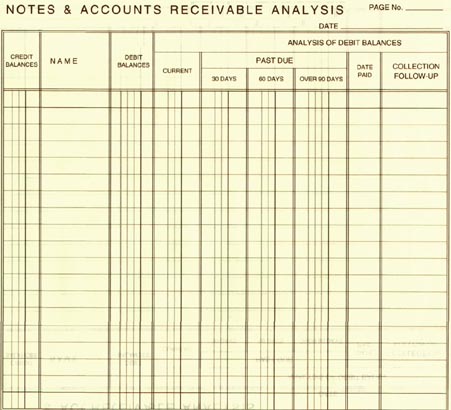

NOTES AND ACCOUNTS RECEIVABLE ANALYSIS |

|

At the end of each month, an aging schedule of all receivables is prepared and reconciled to the balances shown in the appropriate general ledger control accounts. A copy of the schedule, with comments as to the action taken to collect past due accounts is forwarded to the dealer for review. The schedule should show the following:

|

FORD RECEIVABLES |

|

Ford Receivable—Warranty and Policy Claims At month end, the open claims in the Warranty & Policy Register Journal should be listed and reconciled with the balance in the general ledger control account. Differences should be investigated and appropriate adjustments made. Follow-up should be instituted on claims that are more than 30 and 60 days old. Unpaid claims should be reviewed regularly, with particular attention to those over 60 days old. Unless action is to be taken to resubmit denied claims, they should be written off. |

|

Ford Receivable—Vehicle Holdback Individual vehicle holdbacks recorded in the new vehicle purchase journal should be checked to the monthly statement received from Ford Motor Company. The statement total should then be reconciled to the general ledger control account. |

|

Ford Receivable—Jobbing Incentive Credits received from Ford Motor Company should be checked against claimed amounts recorded in Account 1160, Ford Receivable—Jobbing Incentive. The receivable account should be adjusted for differences between amounts claimed and credits received. |

|

Ford Receivable—Floor Plan Allowance Monthly statements from Ford Motor Company should be reconciled with the balance in Account 1161, Ford Receivable—Floor Plan Allowance. After reconciling the statement with the balance in Account 1161, adjustments should be recorded for remaining differences. |

|

Ford Receivable—Extended Service Plan Monthly Warranty & Policy settlement statement from Ford Motor Company should be reconciled with the balance in Account 1164, Ford Receivable—Extended Service Plan. |

|

Ford Receivable—Preparation and Conditioning Credits received from Ford Motor Company should be checked against claimed amounts recorded in Account 1165, Ford Receivable—Preparation and Conditioning. |

|

Finance Company Receivables A separate general ledger control account should be established for each finance company. The detail in the monthly statement from the finance company should be checked to the dealership records, and the statement balance should be reconciled to the general ledger control account balance. |