| INVENTORIES |

|

|

VEHICLES

|

|

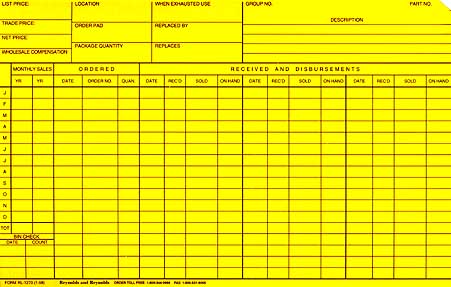

A vehicle inventory record card, not necessarily the one illustrated below, is prepared for each new and used vehicle placed in inventory. At each month end, a listing of vehicles in inventory should be prepared showing the date received, stock number, inventory value of the unit and the applicable floor plan note. The inventory and floor plan notes payable totals should be reconciled to the respective general ledger control accounts. A physical inventory of vehicles should be taken monthly, using the listing to identify each vehicle by stock number.

Review new and used vehicle record forms with your Forms Representative and select the record card you find best fits your needs.

|

INVENTORY RECORD CARD—NEW AND USED (EXAMPLE)

|

|

|

VEHICLE INVENTORY NUMBERING SYSTEM

|

| The following vehicle numbering system is recommended: |

|

Mustang |

Crown Victoria |

Thunderbird |

Light Truck |

Merc. |

Linc. |

Used Car Purchases |

| New |

M-1 |

CV-1 |

TB-1 |

LT-1 |

M-1 |

L-1 |

|

| Second trade |

M-1A |

CV-1A |

TB-1A |

LT-1A |

M-1A |

L-1A |

|

| Used car purchased |

M-1B |

CV-1B |

TB-1B |

|

M-1B |

L-1B |

|

| First trade on used car purchased |

|

|

|

|

|

|

P-1 |

| First repossessed car |

|

|

|

|

|

|

P-1A |

| First trade on repossession |

|

|

|

|

|

|

R-1 |

| |

|

|

|

|

|

|

R-1A |

| Suggested code letters for other new vehicle lines should be clearly understood and the sequence of new vehicle numbers should start over at number one each model year. |

PARTS

|

| 1. |

Issuance of Parts

- Parts to be used by the repair shop or body shop should be issued by parts countermen only upon presentation of a repair order signed by the customer, or in the case of internal work, the authorizing individual.

- Parts issued on a repair order should be listed on the repair order in the section provided.

- Unauthorized persons must not have access to the parts department area, including the loading dock.

|

| 2. |

Costing of Parts Sales

- It is recommended that parts sales be costed on an item-by-item basis at the time of sale. This method produces the most accurate cost of sale data and provides the best accounting control of inventory. It helps to prevent differences between physical counts and book inventory balances arising from costing differences.

- Sales of parts acquired from Ford Motor Company should be costed at current Ford Parts catalog costs. Sales of parts bought from others at a favorable price are costed, where practicable, at the amount paid for the parts other than at catalog prices. Separate inventory accounts are provided for Ford, Lincoln-Mercury, and other-make parts, to make it easier to identify overages and shortages when favorable parts purchases are made.

- Occasionally a dealer will cost his parts sales on a percentage basis. The suggested retail selling prices of various sales categories and percentages used should be verified by test checks of actual item costs over a 30-60 day period every six months. Percentages should then be adjusted to actual. Under this method, when discounts are given, it is necessary to record both the suggested retail price and the actual selling price.

|

| 3. |

Physical Inventories of Parts

- At least once each year, parts on hand should be physically inventoried. It is usually preferable that the inventory be taken by an outside inventory service. If taken by dealership employees, the office manager should see that necessary audit steps, such as testing inventory counts, pricing, extensions, footings, etc., are taken to provide assurance that valuation of physically inventoried parts is accurate.

- After a physical inventory cut-off date is established, account and stock records should be handled in a manner that assures inclusion of all business up to the point of cut-off. Also, business subsequent to the cut-off date should be segregated to prevent inclusion in the cut-off balances.

- Stock records should be adjusted to reflect the physical counts and book records should be adjusted to reflect the valuation of the physical inventory.

|

|

PARTS INVENTORY RECORD

|

|

If an automated inventory control system is not used, a perpetual inventory record card should be maintained for each part number in stock.

|

LABOR IN PROCESS

|

|

The total cost of labor incurred on open repair orders in process at the end of each month represents the inventory of labor in process. The account balance is adjusted to this total each month and is supported by a schedule showing the repair order numbers and labor amounts.

|

SUBLET REPAIRS

|

|

All sublet purchases are charged to the sublet inventory account. THE INVENTORY IS RELIEVED AT THE TIME THE SUBLET WORK IS BILLED TO THE CUSTOMER. A list of open sublet inventory items (unbilled sublet work purchased) is prepared at month end and compared with the general ledger control account after analysis to determine that adjustment is proper. The control account is then adjusted for the difference between the account balance and the inventory listing. To maintain proper control over sublet inventory, a purchase order is prepared authorizing each sublet repair. The customer repair order number is entered on the purchase order, and the vendor’s invoice shows the purchase order number. Before payment, the invoice is cross-referenced to the customer repair order.

|

BODY SHOP MATERIALS

|

|

Purchases of body shop materials are recorded in Account 1442, Inventory—Body Shop Materials. The inventory is relieved based on the estimated usage of body shop materials recorded on body shop repair orders. A physical inventory is taken monthly and book balances adjusted to the physical counts. Consistent differences between book and physical inventory would indicate improper costing, material waste and/or pilferage.

|

GAS, OIL, AND GREASE

|

|

Purchase of gas, oil, and grease is recorded in Account 1443, Inventory—Gas, Oil, & Grease. Inventory relief for the cost of oil and grease sold to customers or used internally should be handled through the normal processing of repair orders.

The following controls may be established for gasoline used internally.

- Only authorized persons should dispense gasoline.

- Individuals requesting gasoline should have authorization from their department managers.

- The person dispensing the gasoline should maintain a record similar to the one below.

- At month end, total gasoline dispensed should be costed and distributed to the appropriate expense accounts by means of an entry in the standard entries journal.

- At month end, a physical inventory should be taken of the gasoline, oil, and grease on hand and book balances adjusted to the physical counts.

|

GASOLINE USAGE AND EXPENSE DISTRIBUTION FORM

|

| ILLUSTRATION NOT AVAILABLE

|

|