Office Management |

| ACCOUNTABLE DOCUMENTS | ||

|

|

||

|

|

||

CONTROL OVER ACCOUNTABLE DOCUMENTS |

||

|

Control over the forms involved in the sale, purchase, receipt and disbursement of assets is fundamental to the system of internal control. The forms listed below are considered as accountable documents and are listed in two categories. These forms should be prenumbered for reference and control purposes.

Responsibility for ordering, receipt, storage and issuance of all accountable documents should be assigned to the office manager, who should designate one of his employees as accountable documents clerk. Wherever possible, if consistent with the size of the dealership, the accountable documents clerk should have no other duties connected with the cash, billing, receivables and payables functions. Unissued documents should be kept under lock, accessible only to the accountable documents clerk. Accountable documents not used within the accounting department should be issued in blocks in numerical sequence to department managers, who should be held responsible for their custody and use. Quantities issued usually do not exceed one week’s supply. As a general rule, check forms should be entered in numerical sequence in the cash disbursements journal or Payroll Journal, as appropriate. The numerical sequence of checks entered can be observed through inspection of the journals; however, the prompt performance of a bank reconciliation is the principal control over unrecorded or unauthorized issuance of checks. With respect to sales and receipt forms, an added control is necessary to help insure that the proceeds of all sales and cash receipts transactions are properly recorded. A check sheet, as illustrated later in this section, should be used to record each of the above-listed sales and receipt forms issued and used. Documents should be used and entered in the journals in numerical sequence, to the extent possible. Documents should not be cleared on the check sheet until they have been recorded in the journals. The date of recording in the applicable journal should be recorded on the check sheet beside the appropriate document number. The check sheet should be reviewed at least weekly for documents that have not cleared. Missing documents should be followed up actively and promptly to prevent cash or other assets from being diverted from the dealership. The approval of a designated member of dealership management should be required before the search for a missing document is discontinued. |

||

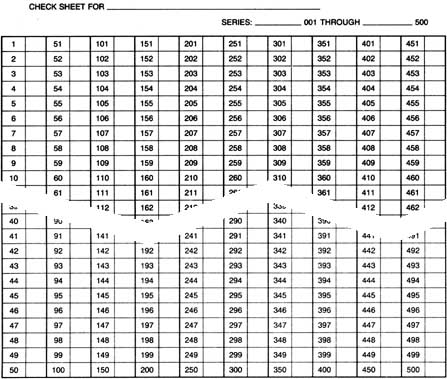

ACCOUNTABLE DOCUMENT CHECK SHEET |

||

|

Space is provided at the top of the form for entry of the document name and the first digits in the prenumbered series. The body of the form shows the last three digits and each side of the form can accommodate 500 document numbers. When not in use this should be filed so no one has access to it except authorized persons.

|